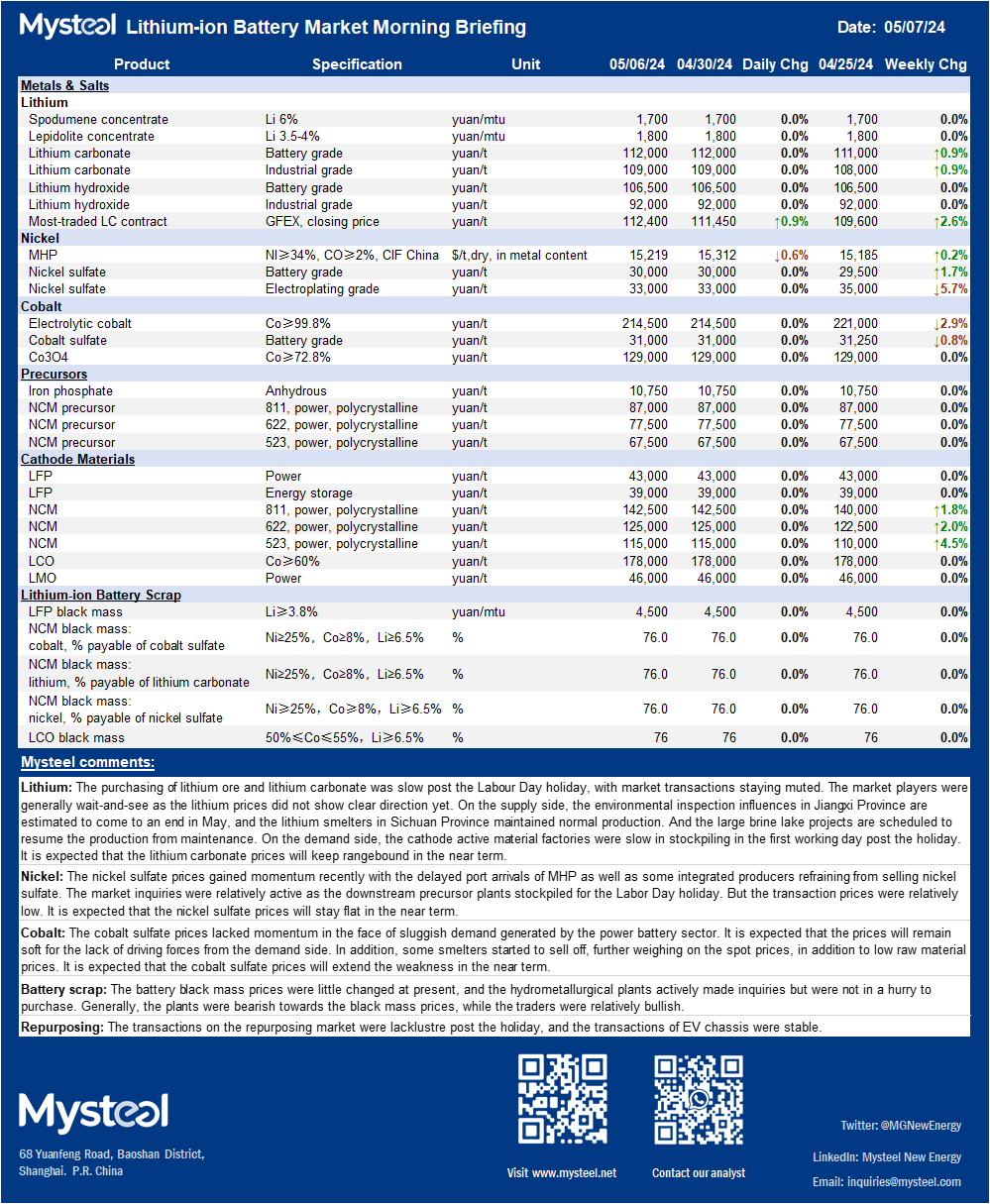

Lithium: The purchasing of lithium ore and lithium carbonate was slow post the Labour Day holiday, with market transactions staying muted. The market players were generally wait-and-see as the lithium prices did not show clear direction yet. On the supply side, the environmental inspection influences in Jiangxi Province are estimated to come to an end in May, and the lithium smelters in Sichuan Province maintained normal production. And the large brine lake projects are scheduled to resume the production from maintenance. On the demand side, the cathode active material factories were slow in stockpiling in the first working day post the holiday. It is expected that the lithium carbonate prices will keep rangebound in the near term.

Nickel: The nickel sulfate prices gained momentum recently with the delayed port arrivals of MHP as well as some integrated producers refraining from selling nickel sulfate. The market inquiries were relatively active as the downstream precursor plants stockpiled for the Labor Day holiday. But the transaction prices were relatively low. It is expected that the nickel sulfate prices will stay flat in the near term.

Cobalt: The cobalt sulfate prices lacked momentum in the face of sluggish demand generated by the power battery sector. It is expected that the prices will remain soft for the lack of driving forces from the demand side. In addition, some smelters started to sell off, further weighing on the spot prices, in addition to low raw material prices. It is expected that the cobalt sulfate prices will extend the weakness in the near term.

Battery scrap: The battery black mass prices were little changed at present, and the hydrometallurgical plants actively made inquiries but were not in a hurry to purchase. Generally, the plants were bearish towards the black mass prices, while the traders were relatively bullish.

Repurposing: The transactions on the repurposing market were lacklustre post the holiday, and the transactions of EV chassis were stable.